Understanding Commercial General Liability Policies

Small businesses make up 99 percent of businesses in California, employing nearly half of the state’s employees. Businesses of all sizes, however, rely on commercial general liability (CGL) insurance to protect against bodily injury and property damage claims, personal and advertising injury, and medical claims outside of lawsuits. The coverage usually pays for medical and legal expenses, and monetary losses and property damage or losses.

Like automobile comprehensive coverage, CGL insurance is capped, often at $500,000 or $1 million, and the insurer won’t pay beyond that amount. In addition, just like auto insurance, the underwriting company can and will often challenge a claim being made. Insurance companies are, after all, for-profit enterprises and it is in their best interest to challenge their policyholders’ filings.

If your business in or around Irvine, California, is in a dispute with a commercial general liability insurer over a claim—or has had a claim denied—contact William B. Hanley, Attorney at Law. With more than 40 years of business and commercial litigation experience, Attorney William B. Hanley has helped businesses of all sizes recover the compensation due them under general liability insurance and other policies. He proudly serves clients throughout Orange, Los Angeles, and San Diego counties.

Overview of Commercial General Liability Insurance

The Golden State has no law requiring a business to have commercial general liability insurance, but it is certainly a standard practice and a wise decision. Otherwise, your company—and you personally unless your business is a corporation or limited liability company (LLC)—will be responsible for any claims arising from the operations of your enterprise.

The California Attorney General’s website notes: “There are three primary coverage sections that make up a CGL policy: premises liability, products liability and completed operations.” Completed operations means property damage or bodily injury occurring after your work has been completed; for instance, after you have installed a spa tub in a customer’s home. Libel and slander lawsuits resulting from advertising or other actions are also generally covered.

Types of Liability Coverage

The CGL policy you purchase will generally be of two types: claims-made and occurrence. Claims-made coverage means that your policy will apply to any claim, regardless of when the injury or loss occurred, that is made during the time the insurance policy is in effect. Occurrence means that the policy will cover only losses or injuries that occur during the time of the policy, even if the claim is made at a later date.

What CGL Covers

A commercial general liability policy will generally cover:

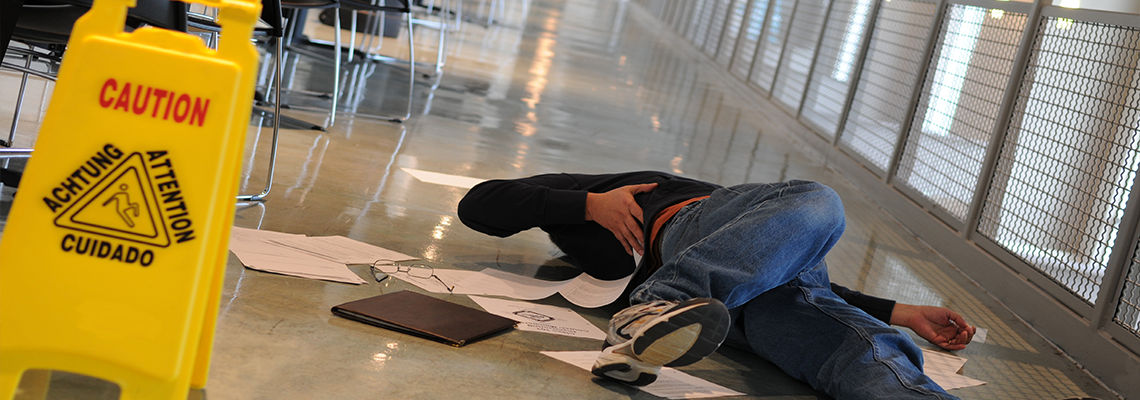

BODILY INJURY: Your employees will be covered by your workers’ compensation insurance, but if a non-employee is injured on your premises or as a result of your product offerings or completed work, the CGL policy should cover that.

PROPERTY DAMAGE: Your CGL should also cover damage to a customer’s or client’s property due to conditions on your premises or as a result of a product offering or completed-work situation.

PERSONAL OR ADVERTISING INJURY: Damage to someone’s rights or reputation is also covered by CGL policies, including acts such as libel, slander, copyright infringement, invasion of property or privacy, and more. If your advertising results in any sort of losses such as for false promises, that should be covered as well.

What CGL Does Not Cover

A commercial general liability policy does not cover intentional or expected damage by the insured. It does not cover, according to the State Attorney General, “intentional injury; insured contracts; liquor liability; workers’ compensation and employers’ liability; pollution; aircraft; automobile; watercraft; mobile equipment; war; care, custody, and control; damage to your work; impaired property; sistership liability; and failure to perform.”

Why Are CGL Claims Denied?

Insurers being insurers, they can be expected to challenge, limit, or even deny claims made by policyholders. Typical reasons cited for a denial of your claim include:

The claim was not timely

The injury was not covered by the insurance policy

The insurer suspects fraud

Coverage limits have been met or exceeded

If your claim is denied, you can file an appeal, and if that fails, you may be able to take the matter to court. You can charge the insurer with bad faith tactics for prioritizing its interests over yours as the policyholder.

Speak with an Experienced Attorney

If you are running into resistance by your CGL insurer, or worse, have had a claim denied, you need to reach out for experienced and knowledgeable legal assistance. Uphold your rights under the terms of the policy you’ve purchased. For legal help in or around Irvine, California, and throughout the Southern California area, contact William B. Hanley, Attorney at Law.